~9000 BC—Barter & Commodity Money

Every transaction was a negotiation, and most of them failed. You had grain; I had cattle. Unless I wanted grain and you wanted cattle at the exact same moment, no deal. Economists call this the double coincidence of wants. Everyone else just called it life. There was no unit of account, no way to save for the future, no way to trade with a stranger two valleys over. This single friction — the absence of money — capped the complexity of human civilization for thousands of years. We could build villages but not cities. We could feed families but not armies. Money wasn't invented because someone had a clever idea. It was invented because without it, we were stuck.

~5M humans. No civilizations yet — scattered proto-settlements.

~3000 BC—Rai Stones of Yap

Here is the most underrated monetary innovation in history, and it happened on a tiny island in Micronesia. The people of Yap used massive limestone discs — some over 12 feet across — as money. Each stone was quarried 250 miles away in Palau and hauled back by canoe. Men died making the trip. That was the point: the value of each stone was the labor and risk embedded in it. A proof-of-work token, thousands of years before Satoshi. But the truly radical part wasn't the stones — it was the ledger. Most were too heavy to move, so ownership was tracked by oral consensus. Everyone simply knew who owned which stone. One famous disc sank to the ocean floor during transport and kept circulating as currency, because the community still agreed on who owned it. Money that doesn't need to move. A shared record maintained by social consensus rather than a central authority. Sound familiar?

~600 BC—First Coins Minted

This is where money becomes money. In the Kingdom of Lydia — modern-day western Turkey — King Alyattes stamps a lion's head onto small discs of electrum, a natural gold-silver alloy from the Pactolus River. The royal seal guarantees weight and purity. For the first time in human history, you can hand a stranger a piece of metal and both of you know exactly what it's worth. No weighing. No haggling over quality. No trust required. The idea is so obviously superior that it spreads like a virus. Within a generation, Greek city-states, Persia, and India are all minting their own coins. Commerce explodes. Markets emerge. Trade routes stretch across continents. Standardized coinage doesn't just simplify trade — it makes civilization at scale possible. Every empire that follows will be built on coins. And every empire that falls will fall, in part, by debasing them.

~300 AD—Rome Debases Its Currency

The Roman denarius started at 98% pure silver. It ended as a bronze slug with a silver wash. The decline took centuries, but the playbook was established in the first act. When Rome's military ambitions outgrew its treasury, emperors discovered the oldest trick in monetary history: stamp the same face value on a coin with less metal in it. Under Nero, silver content dropped to 94%. Under Septimius Severus, 50%. By Diocletian, less than 5%. Prices rose 1,000% in a century. Soldiers refused to accept the coins and demanded gold or goods. Trade in the provinces collapsed back to barter. The barbarians didn't destroy Rome. Rome destroyed Rome — one diluted coin at a time. Every empire since has repeated this exact pattern. Not one has learned from it.

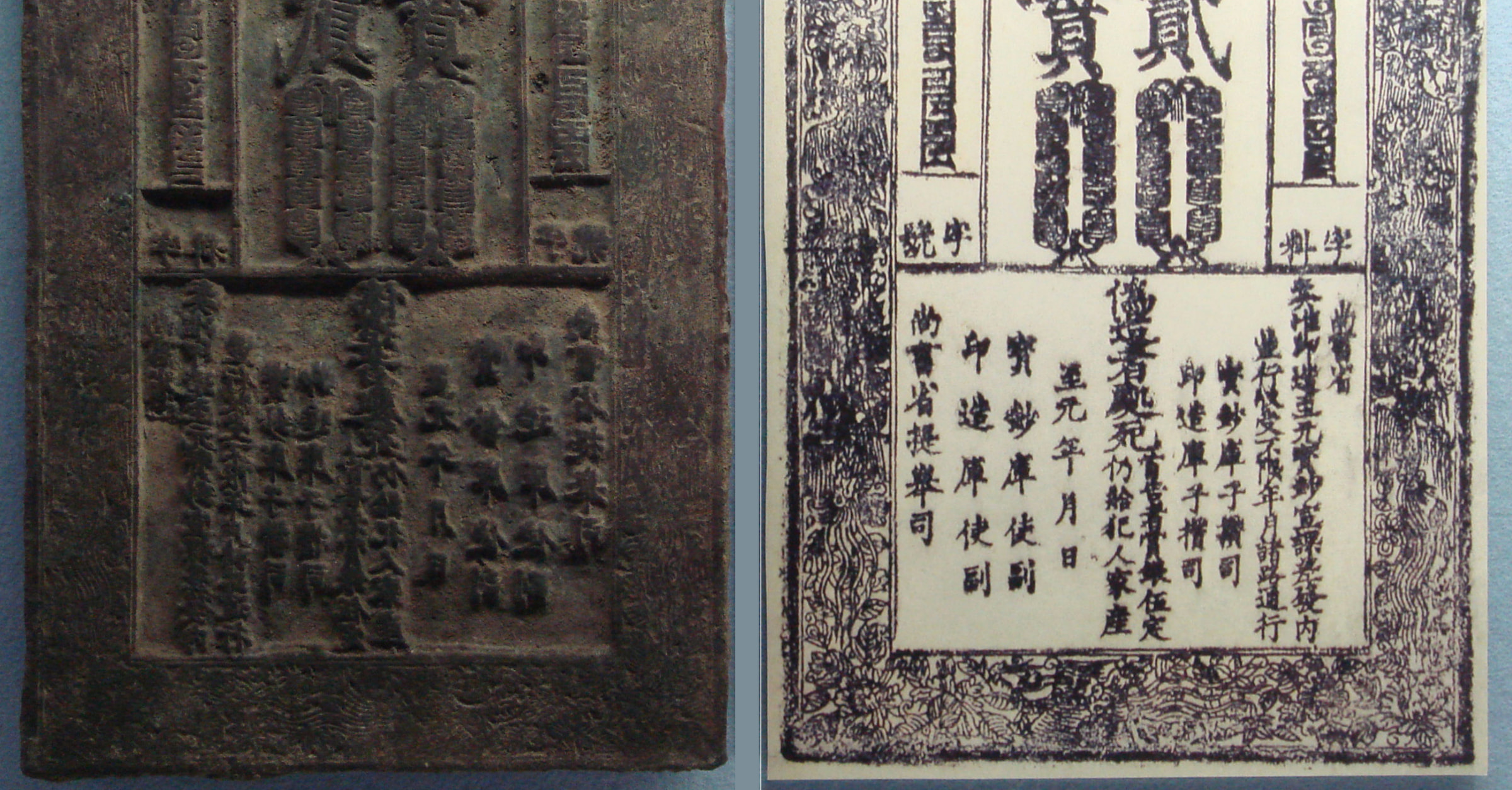

~1000 AD—China Invents Paper Money

The printing press is easy to start and impossible to stop. China proved it first. The Song Dynasty invents jiaozi — the world's first government-issued paper currency. Merchants in Sichuan, sick of hauling heavy iron coins, begin using paper certificates backed by deposits at trustworthy shops. The government takes over issuance, backs each note with iron and silver reserves, and for a while it works brilliantly. Paper money lubricates the most advanced economy on Earth. Then the temptation sets in. Successive dynasties print more notes than reserves can back. The Yuan Dynasty floods the economy with unbacked paper to fund wars and public works. Hyperinflation follows. By the Ming Dynasty, paper money is abandoned entirely, and China returns to silver and copper coins for three hundred years. The whole arc — innovation, adoption, abuse, collapse — plays out a millennium before the Federal Reserve exists. The lesson couldn't be clearer. Nobody learns it.